Weekly Market Commentary – 9/10/2021

-Darren Leavitt, CFA

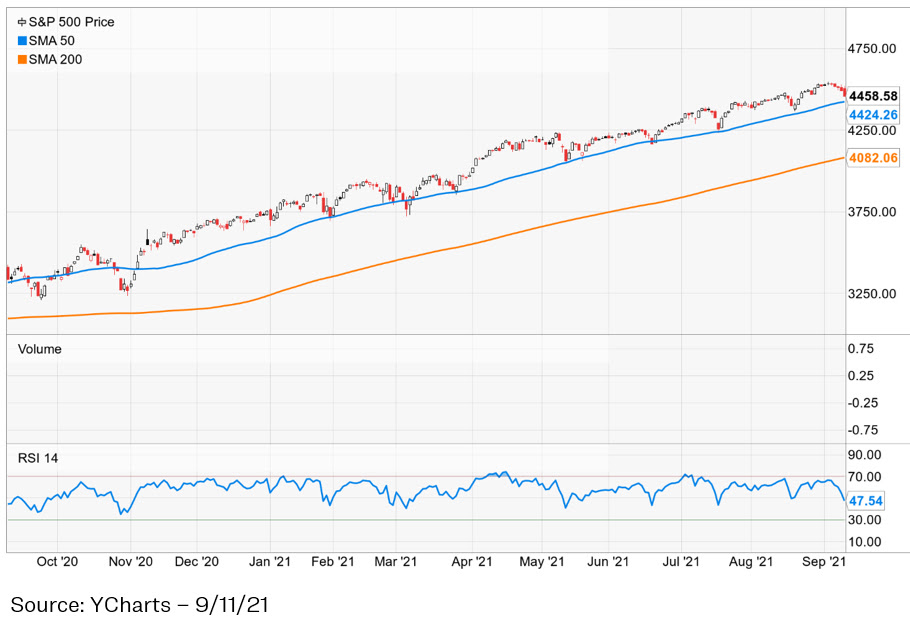

The holiday-shortened week produced negative returns across the board for US equity indices. The month of September has historically been a tough month for equities, and given the outsized moves we have seen so far this year, it is not a surprise to see a bit of a pullback. An early week sell-off in Cryptocurrencies set the stage for other risk assets. Bitcoin started the week at $52,791, then tumbled 13% to close on Friday at $45,605. Goldman Sachs was the third investment bank in a couple of weeks to reduce their growth outlook for the US, which further dampened market sentiment. In Europe, the European Central Bank announced that it would curtail its asset purchase program at a very measured pace and on a vague timeline. In Washington, the Infrastructure spending bill continued to be up for debate even as the Democrat Senator from West Virginia, Manchin, partially pulled his support for the proposed human infrastructure component of the bill. Economic data was light on the week but showed another strong print in the Producers Price Index and continued progress on the labor market.

For the week, the S&P 500 lost 1.7%, the Dow gave up 2.2%, the NASDAQ shed 1.6%, and the Russell 2000 lagged with a loss of 2.8%. US Treasuries sold off slightly for the week. The 2-year yield increased one basis point to 0.21%, while the 10-year Note yield increased two basis points to close at 1.34%. Gold prices fell just over 2% or $41.70 to close at $1792 an Oz. Oil prices increased fractionally, gaining $0.60 to close at $69.75 a barrel.

On a year-over-year basis, the Price index for final demand was up 8.3% as the headline PPI for August came in at 0.7%, a bit higher than the expected 0.6%. Initial Jobless Claims fell to the lowest level since the pandemic’s start, coming in at 310K versus an expected 337k. Continuing claims fell to 2.783 million on a week where supplemental federal unemployment benefits expired. Next week we will get a look into consumer prices with the CPI. We will also get August Retail Sales and the first September reading of the University of Michigan’s Consumer Sentiment survey.

Investment advisory services offered through Foundations Investment Advisors, LLC (“FIA”), an SEC registered investment adviser. FIA’s Darren Leavitt authors this commentary which may include information and statistical data obtained from and/or prepared by third party sources that FIA deems reliable but in no way does FIA guarantee the accuracy or completeness. All such third party information and statistical data contained herein is subject to change without notice. Nothing herein constitutes legal, tax or investment advice or any recommendation that any security, portfolio of securities, or investment strategy is suitable for any specific person. Personal investment advice can only be rendered after the engagement of FIA for services, execution of required documentation, including receipt of required disclosures. All investments involvement risk and past performance is no guarantee of future results. For registration information on FIA, please go to https://adviserinfo.sec.gov/ and search by our firm name or by our CRD #175083. Advisory services are only offered to clients or prospective clients where FIA and its representatives are properly licensed or exempted.